TCFD REPORT 2023

TASK FORCE ON

CLIMATE-RELATED

FINANCIAL DISCLOSURES

REPORT 2023

Thai Beverage Public Company Limited

CLIMATE-RELATED

FINANCIAL DISCLOSURES

REPORT 2023

Thai Beverage Public Company Limited

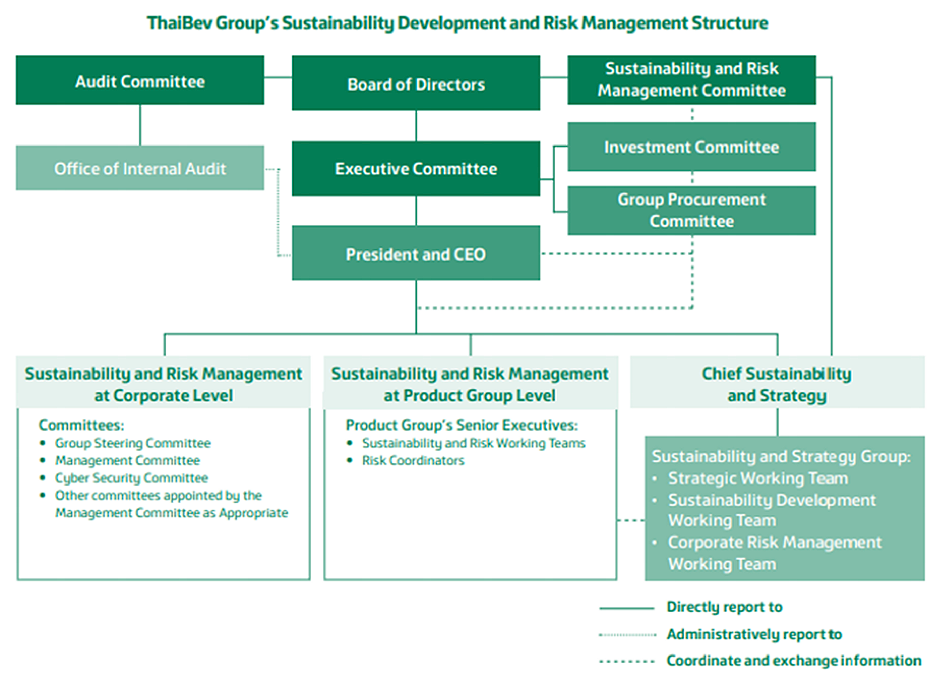

Figure 1: ThaiBev’s Climate-related Governance Structure

| ThaiBev’s Function | Climate-related Roles and Responsibilities | Meeting Frequency |

| Board of Directors |

|

Quarterly |

| Sustainability & Risk Management Committee (SRMC) |

|

Quarterly |

| ThaiBev’s Function | Climate-related Roles and Responsibilities | Meeting Frequency |

| Executive Committee |

|

Monthly |

| President and Chief Executive Officer (CEO) |

|

Quarterly (With the SRMC) |

| Chief Sustainability and Strategy |

|

Quarterly or as necessary |

| Sustainability and Strategy Group | Sustainability Development Working Team (SDWT)

|

Bi-monthly |

| Investment Committee |

|

As necessary |

Table 3: ThaiBev Physical Risk Scenario Analysis Parameters

| Purpose | To analyze whether physical related risks (both acute and chronic) have a significant impact on ThaiBev’s business in the future, and the mitigation measures/adaptation plan required for significant risks. |

| Scenarios | SSP1-2.6/ RCP 2.6: A low emissions pathway limiting warming to below 2 °C. SSP2-4.5/ RCP 4.5: An intermediate emissions pathway where global temperature rises by 2.5 - 3 °C. SSP3-8.5/ RCP 8.5: High emissions. A pathway that represents a baseline where no additional mitigation measures are implemented, assuming that increase in temperature will be about 4.3 °C by 2100 |

| Scenario time horizons |

|

| Scope of assessment | 57 facilities in Thailand, Vietnam, Scotland, Myanmar, and Cambodia, accounting for 100% of the total number of facilities. |

| Target area of financial analysis | Operations and supply chain, transportation disruptions from factory to distributed dealers.* |

Table 4: ThaiBev Physical Risk Scenario Analysis Parameters

| Climate Physical Risks | Timeframe | Impact | Description | Adaptation Measures* | |

| Acute | |||||

| Extreme Rainfall | Medium term (3-10 years) | Medium to high | The extreme precipitation events, such as one-day maximum rainfall and number of days with heavy rainfall, are likely to increase the probability of floods causing damage to ThaiBev’s assets and increasing the costs of production due to supply chain disruptions. | ThaiBev conducted a flood risk assessment in areas prone to flooding for all key assets, and highlighted areas that were the most likely to be affected. To mitigate any impacts ThaiBev constructed flood barriers, storm water draining, or pumping stations in the areas highlighted. Further, alternative transportation routes are planned to minimize supply chain disruption due to potential floods. Each production site tracks and monitors the weather forecast including the storm and earthquake reports from the Thai Meteorological Department to receive the earliest warnings. All production sites shall ensure that the external roofing or solar rooftop systems are in adequate condition and implement response mechanisms to reduce impacts during the storms. |

|

| Wind Storm | Medium term (3-10 years) | Medium to high | Greater probability of disruptions within the operations, supply chain, and finished goods inventory due to storms. | ||

| Chronic | |||||

| Water Stress | Long term (>10 years) | Medium to high | Changes in water availability can affect ThaiBev’s production lines, supply chain, and revenue, especially when factories operate in high water stress areas. | ThaiBev has initiated the Water Sustainability Assessment (WSA) for both surface water and groundwater, which covers all production sites, in order to conduct an in-depth assessment of present and future risks and opportunities. The assessment has led to the development of Integrated Water Resources Management Plan (IWRM) for each assessed factory, focusing on implementing a long-term adaptation and mitigation plan. |

|

| Sea Level Rise | Long term (>10 years) | Low to medium (for coastal locations) | Seawater intrusion into natural water sources such as rivers and aquifers can cause disruption to ThaiBev’s production, leading to more spending on the operational cost of buying fresh water. ThaiBev’s assets located in coastal areas may be impacted, resulting in increased costs of production as well as supply chain disruptions. |

Seawater intrusion into aquifers: ThaiBev will engage with local communities and governmental authorities near the identified high-risk areas to improve the groundwater wells. Seawater intrusion into rivers: Expand freshwater stock facilities and implement a management plan to ensure sufficient fresh water supply by using water saving technology, water recycling systems, and rainwater harvesting systems. Adaptation measures for coastal floods are drawn from our adaptation measures for riverine flood risks. |

|

| Increasing Temperature | Long term (>10 years) | Low to medium | Changes in air temperature will decrease crop yields throughout ThaiBev’s supply chain, which may cause a higher cost of material sourcing. | ThaiBev has continued the educational and training initiative with farmers to help conserve resources, prepare for natural disasters and adopt technology for production efficiency. | |

Table 5: Key Assumptions Applied to Flooding Financial Impact Quantification

| Flood Depth | Impact Level | Flooding Occurrence (times per year) | Flood Duration (days per incident) | ||

| SSP5-8.5/ RCP 8.5 | SSP2-4.5/ RCP 4.5 | SSP1-2.6/ RCP 2.6 | |||

| >0.5m | High | 2 | 1 | 0 | 5 |

| 0.15m < X < 0.5m | Medium | 2 | 1 | 0 | 3 |

| < 0.15m | Low | 2 | 1 | 0 | 0 |

Remarks:

|

Table 6: Flooding Scenario Analysis Risk Level and Financial Impact Results

| Scenario | Probability | Severity (S) at 2030 | Risk Level at 2030 | Financial Impact (Million THB) | ||||||||

| % | Level | % | MTHB | Level | MTHB | Level | Spirit | Beer | Food | NAB | Total | |

| Scenario 1: High emissions SSP5-8.5/ RCP 8.5 |

20% | Unlikely | 0.00% | 3.51 | Insignificant | 0.70 | Low | 3.19 | 0.00 | 0.00 | 0.32 | 3.51 |

| Scenario 2: Intermediate emissions SSP2-4.5/ RCP 4.5 |

50% | Medium | 0.00% | 1.64 | Insignificant | 0.82 | Low | 1.44 | 0.00 | 0.00 | 0.20 | 1.64 |

| Scenario 3: Low emissions SSP1-2.6/ RCP 2.6 | 30% | Unlikely | 0.00% | 0.00 | Insignificant | 0.00 | Low | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 |

| Financial impact and risk level for each product group | 1.36 | 0.00 | 0.00 | 0.16 | 1.52 | |||||||

| Low | Low | Low | Low | Low | ||||||||

| Impact to Profit | Risk Level |

| 0 – 20 Million THB | Low |

| 20 – 100 Million THB | Medium |

| 100 – 500 Million THB | High |

| 500 – 2,000 Million THBB | Very High |

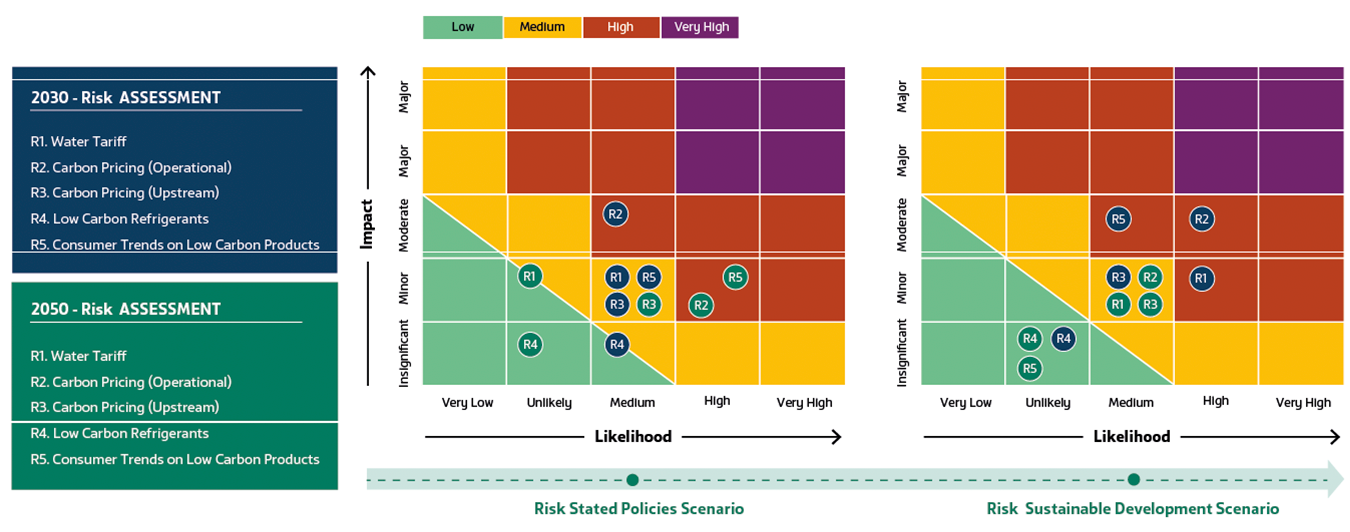

Table 7: ThaiBev’s Transition Risk and Opportunity Scenario Analysis (2022-23)

ThaiBev has identified a list of transition risks and opportunities that are considered relevant and are used in scenario analysis:| Purpose | To analyze whether transition related drivers (policy/legal, market, technology, reputation) have a significant impact on ThaiBev’s business in the future, and what risk mitigation actions are required for significant risks. |

| Scenarios |

|

| Scenario Time Horizons |

|

| Target area of analysis | Operations and value chain |

| Scope of financial impact calculations | ThaiBev Group |

| Risk Category | Opportunity Category | ||

| Policy and Legal | Water Tariff: possibility of increased production costs of beverage products caused by an increased water tariff in Thailand. | Technology Advances | Material Circularity: increasing financial feasibility of recycling technologies where recycled materials become cheaper than virgin materials. |

| Carbon Pricing (operational and upstream): carbon pricing policies that are already in place in markets of ThaiBev’s supply chain and expected policies in operational areas. | Resource Efficiency: utilizing/ investing in energy efficient and emissions reduction technologies/ machineries to potentially reduce future costs. | ||

| Market Changes | Consumer Trends on Low Carbon Products: changing consumer and market preferences towards products seen as better for the environment | Market Changes | Development of Low-Carbon Products: ThaiBev increasing the share of products that receive an approval for the Carbon Footprint of Products and Carbon Footprint Reduction Label. |

| Reducing Costs of Renewable Electricity: due to increased demand from the marketplace and economies of scale while investing in these materials. | |||

| Technology Advances | Low Carbon Refrigerants: emergence of new refrigerants with lower global warming potential to replace existing refrigerants. However, no material risk from high emission refrigerants and climate-related reputation is identified due to less exposure and usage. | Reputation | Stakeholder Sentiment: increased stakeholder expectations on climate action, especially amount investors, shareholders, consumers, and societal expectations. |

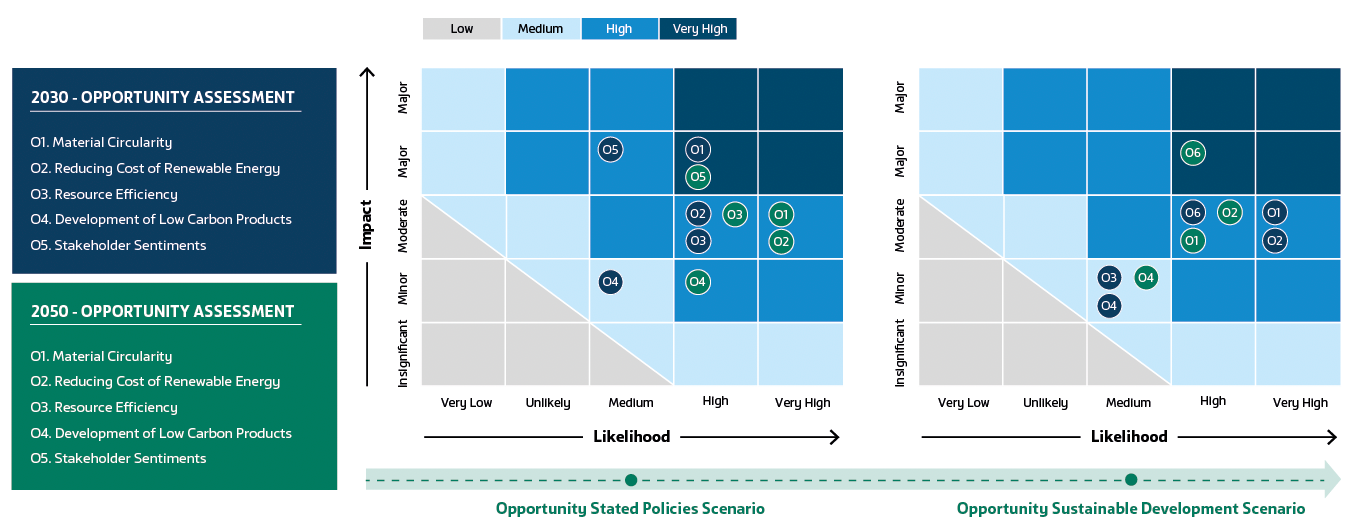

Figure 3: Results of Transition Opportunities Scenario Analysis

Figure 4: Results of Transition Risks Scenario Analysis Table

Consequently, ThaiBev dived deeper into higher priority and most material transition risks and opportunities, as presented in Table 8.

Table 8: Scenario Drivers, Business Impacts, and Response Measures

| Driver | Timeframe | Business Implications (Impact to Business) | Response Measures |

| Carbon Pricing (operational and value chain) | Medium term (3-10 years) | The application of carbon-pricing in Thailand would mean a company with high emissions would bear more operation costs, potentially affecting ThaiBev in the following ways:

|

|

| Water Tariff | Short term (0-3 years) | Thailand is in the process of developing a water tariff, according to the Water Resources Act, B.E. 2561 (2018). The level of expected impact is subject to the amount of water consumption and agreed upon national regulations on the water tariff. It is assumed that tariff rates increases may not be frequent and that Thailand may be less impacted by on droughts due to the government’s active strategy and mitigation measures. Nonetheless, increasing investment costs in innovation for water efficiency are expected. |

|

| Consumer Trends on Low Carbon Products | Medium term (3-10 years) |

|

|

| Material Circularity | Short term (0-3 years) | Thai Beverage Recycle Co., Ltd. (TBR) focuses on adding more value to recycled and waste materials to supply the group companies and external clients. This action aligns with the national strategy of the Bio-Circular-Green Economic Model, which aims to maximize resources efficiency and circular to assist business growth.

|

|

| Reducing Cost of Renewable Energy | Medium term (3-10 years) |

|

|

| Shareholder and Stakeholder Sentiment | Medium term (3-10 years) |

|

|

Table 9: Carbon Tax Scenario Analysis Risk Level and Financial Impact Results

| Scenario | Probability | Severity at 2030; | Risk Level at 2030 | Financial Impact (Million THB) | ||||||||

| % | Level | % | MTHB | Level | MTHB | Level | Spirit | Beer | Food | NAB | Total | |

| Scenario 1: High emissions (STEPS) | 30% | Unlikely | 0.00% | 0 | Insignificant | 0 | Low | 0 | 0 | 0 | 0 | 0 |

| Scenario 2: Intermediate emissions (APS) | 50% | Medium | 0.45% | 392 | Moderate | 196 | High | 168 | 176 | 24 | 24 | 392 |

| Scenario 3: Low emissions (NZE) | 20% | Unlikely | 1.35% | 1,175 | Very Significant | 235 | High | 505 | 529 | 71 | 71 | 1,175 |

| Financial impact and risk level for product group | 185.27 | 193.89 | 25.85 | 25.85 | 430.87 | |||||||

| High | High | Medium | Medium | High | ||||||||

| Impact to Profit | Risk Level |

| 0 – 20 MB | Low |

| 20 – 100 MB | Medium |

| 100 – 500 MB | High |

| 500 – 2,000 MB | Very High |

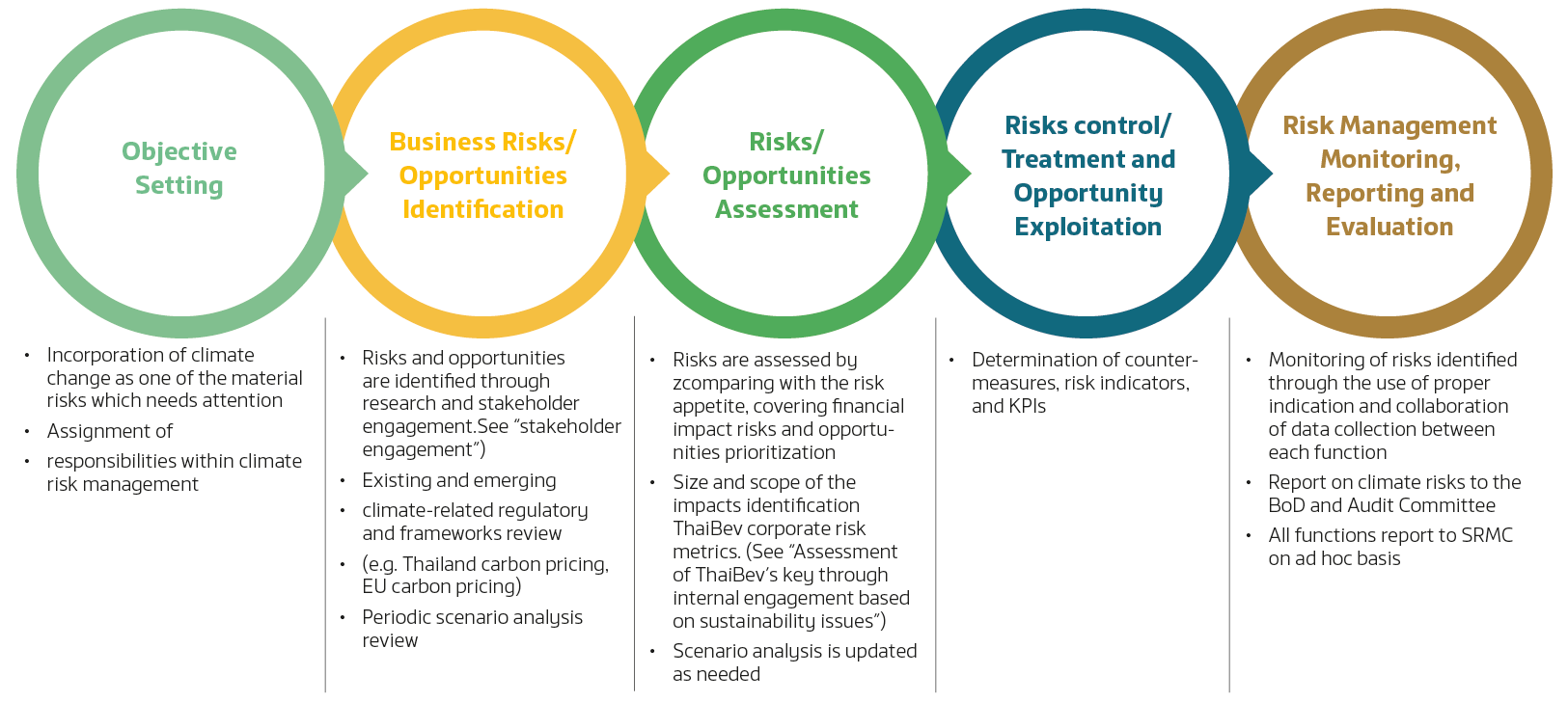

Figure 5: Risk Management Process Relevant to Climate-related Risks and Opportunities

| 2030 Target | Net Zero Targets |

50% renewable energy by 2030 |

|

| Performance | Unit | 2020 | 2021 | 2022 | 2023 |

| Scope 1 GHG emissions | Metric tons CO2e | 1,015,562 | 905,538 | 932,740 | 934,040 |

| Biogenic CO2 emissions | Metric tons CO2e | 398,836 | 422,576 | 456,368 | 441,776 |

| GHG Scope 2 emission | Metric tons CO2e | 292,542 | 276,009 | 322,792 | 273,667 |

| GHG Scope 1 and Scope 2 emission | Metric tons CO2e | 1,308,105 | 1,181,547 | 1,255,532 | 1,207,707 |

| GHG Scope 3 emission | Metric tons CO2e | 741,679 | 1,407,457 | 1,330,365 | 1,967,825 |

Table 11: Climate-related Risks and Opportunities Metrics

| Transition Risk and Opportunity | 2020 | 2021 | 2022 | 2023 |

| Low Carbon Products | ||||

| Revenue from low carbon products (% of total revenue) | 15% | 19% | 8% | 9% |

| Total avoided emissions from low carbon products (tCO2e per year) | 32,529 | 30,253 | 36,633 | 73,700 |

| Number of products with Carbon Footprint of Product (CFP) certification | 105 | 107 | 88 | 91 |

| Number of products with Carbon Footprint Reduction (CFR) certification | 19 | 38 | 47 | 53 |

| Remark: Excludes operations in Vietnam | ||||

| Renewable Energy | Target: To increase the share of renewable energy in energy consumption to 50% by 2030 | |||

| Renewable energy generation (MWh) | 748,633 | 753,034 | 994,007 | 875,506 |

| % of Renewable Energy Consumption out of Total Energy Consumption | 27.6% | 28.5% | 33.4% | 30.8% |

ThaiBev's Sustainability

ENVIRONMENTAL

![]()

SOCIAL